Carbon Limiting Technologies (CLT) has been deeply engaged with industrial heat innovation, particularly in Food & Beverage (F&B). We recognise that decarbonising Scope 1 process heat, the on-site heat used for cooking, boiling, drying, pasteurising, distilling, sterilising, and cleaning, is one of the most intractable challenges facing F&B manufacturers on the journey to Net Zero. The urgency of this challenge has been heightened by the need to reduce exposure to the operational and financial risks of fossil fuel reliance, which have been further highlighted by the current geopolitical climate.

There is a clear decarbonisation “heat gap” in F&B process heat: a range of temperature requirements where low-carbon technologies exist, but are not yet financially viable or commercially ready enough to displace fossil fuel systems at scale. Engineers and site teams working on steam systems and process heat will be familiar with the challenge: integrating new low-carbon heat technologies into live production environments while meeting carbon targets, sustaining operational performance, protecting product quality and satisfying internal return-on-investment hurdles. The ambition to solve this problem exists, but the business case often does not yet clear the hurdle rates for deployment.

CLT’s mission is to help close this gap by working across engineering, R&D, procurement and finance teams to identify, structure, and activate collaborations with innovation, at the right level of maturity and through the right commercial model, to create mutual value through decarbonisation.

Food & Beverage heat decarbonisation is a major industrial challenge

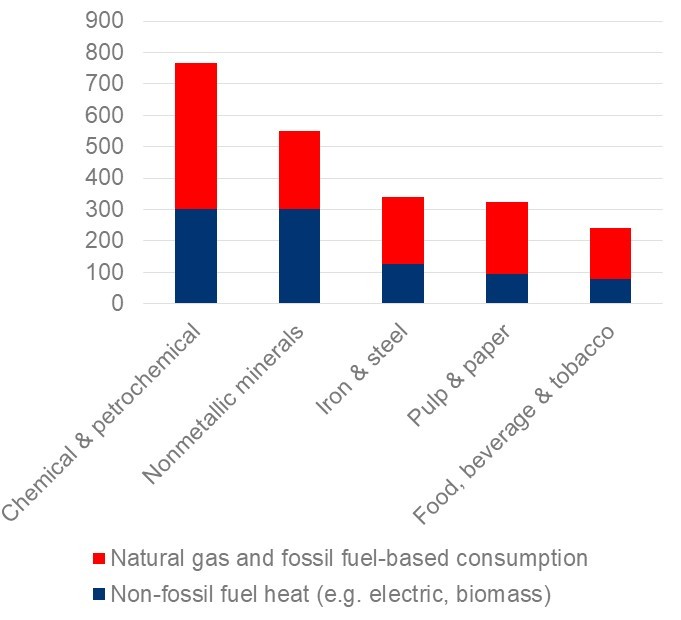

Decarbonising heat in food and beverage manufacturing is a major global industrial challenge. While sectors such as iron and steel often receive greater attention because of their high-temperature heat requirements and concentrated emissions, the scale of F&B heat demand is of a similar order of magnitude in the EU. The challenge is different: rather than a smaller number of very large, high-temperature sites, F&B heat demand is spread across a wide range of manufacturers, processes, ownership structures and temperature requirements.

Interestingly, much of this challenge sits at relatively low temperatures. According to the Renewable Thermal Collaborative, 97% of the heat in the F&B sector is considered to be low-temperature, below 130°C)[1]. Yet a large share of this heat remains fossil-fuelled. Of the approximately 160 TWh of annual heat consumption in the EU F&B sector, 65% is yet to be decarbonised, contributing over 90 million tonnes of CO2-equivalent emissions per year [3]. This makes F&B heat decarbonisation both a significant emissions challenge and a practical deployment challenge, requiring solutions that can work across many different sites and processes.

Where the heat gap emerges, and the lack of viable solutions for full electrification

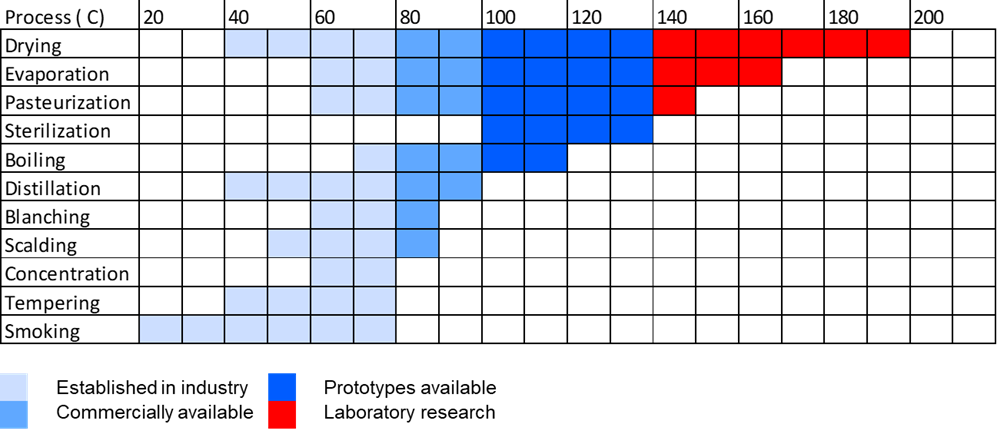

The good news is that electrification and efficiency solutions exist for much of the low- and mid-temperature heat demand. Commercial heat pumps can already supply hot water up to around 80–100°C with COPs of 3–6, drastically reducing emissions as the grid continues to decarbonise. Mechanical vapor recompression (MVR) can efficiently recover and re-compress low-pressure steam (e.g. from evaporators) into useful heat. Heat integration and waste-heat recovery measures can further cut new heat demand, while thermal energy storage (TES) can further improve the economics and carbon case of electrification by enabling flexible energy use as the grid goes green.

The challenge becomes more acute above the 100°C range, where critical F&B processes such as drying, pasteurisation and evaporation sit. In this temperature range, heat pumps are not yet widely commercially available as direct replacements for gas boilers or CHP systems as the main heat generator.

As temperature requirements rise above ~100°C, the efficiency (COP) of available heat pumps falls and fewer mature options exist. Other electric heat generation technologies can technically meet higher temperatures, but also face commercial constraints. Electric boilers can provide steam up to ~180°C+ and are proven technology, but operate at COP ~1, making them expensive to run unless electricity is very low-cost. Direct electric heaters can generate higher-temperature air or fluid heat (even 200 °C+), but face similar cost and power supply hurdles.

This means that, for many F&B manufacturers, the challenge is not whether electrification is the right long-term pathway. It is whether today’s solutions can meet the required temperature, performance and cost thresholds needed for deployment at site level.

The spark gap remains a major barrier. Electricity is often significantly more expensive than natural gas, particularly in the UK, meaning electric heat technologies must achieve sufficiently high efficiency to compete on operating cost. To break even, a heat pump’s COP must exceed the electricity-to-gas price ratio, adjusted for gas boiler efficiency. At lower temperatures, industrial heat pumps can achieve COPs that support a strong business case. At higher temperatures, particularly around 150–180°C, performance is currently lower, so gas boilers often remain cheaper to operate unless power tariffs, carbon costs or technology performance improve.

The economic challenge is compounded by electrical capacity constraints. Replacing large gas boilers with electric systems can materially increase a site’s peak power demand, triggering connection upgrades, on-site electrical works or local network reinforcement. It can also increase exposure to demand charges and other non-energy costs, meaning the economics are shaped not only by the unit price of electricity, but by how electrification changes the site’s overall load profile. This is becoming more material in the UK: a UK Energy Research Centre briefing published in 2025 found that, without further network investment, 42% of large industrial sites could face power constraints by 2030, rising to 77% by 2050, with food and drink identified among the most affected sub-sectors alongside glass, iron and steel, and non-ferrous metals[6].

Other non-technical barriers also slow progress. Operational risk aversion looms large: few F&B plants want to be first movers for new heat technology without robust track records. Integration and downtime concerns are real, particularly where new systems must be introduced into live production environments. Site-specific constraints, including space, electrical supply, hygiene requirements and process control, further complicate retrofits. For high-value or quality-critical processes, reliability is essential.

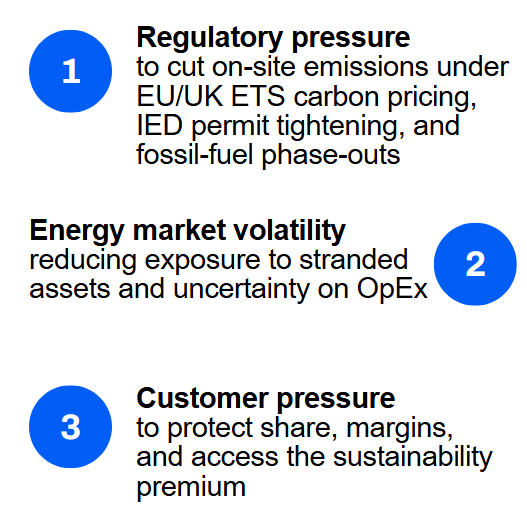

The result is that manufacturers are left exposed on three fronts.

Together, these barriers explain why electrification has not yet scaled across the harder parts of F&B process heat. The issue is not that the technology pathway is absent, but that current solutions do not yet consistently meet the performance, cost and integration requirements needed for widespread deployment.

Demonstrations show the pathway, but scale-up must accelerate

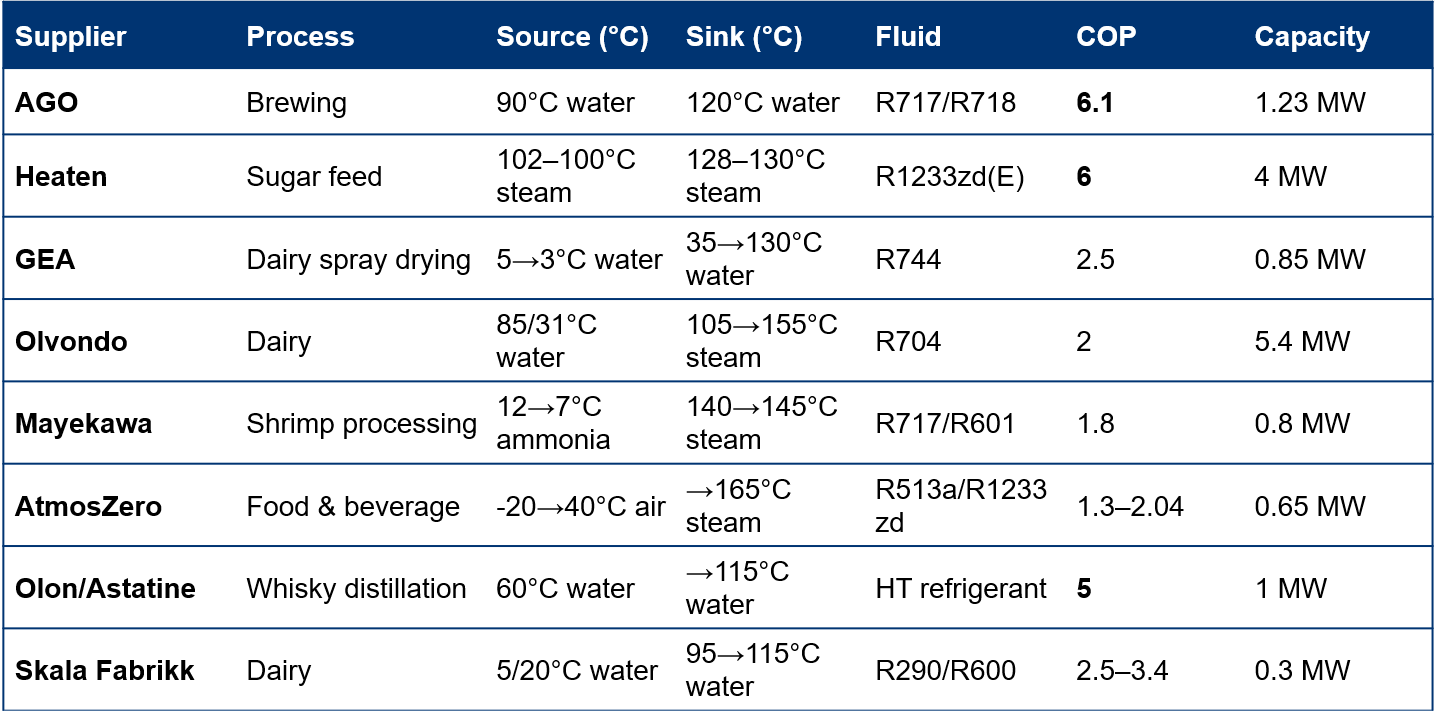

Despite these barriers, full-scale demonstrations in commercial settings show that higher-temperature electric heat can work in F&B processes. Trials identified through IEA Project 68 have shown that heat pumps can electrify energy-intensive applications, including brewing, dairy, sugar processing and distillation, with COPs that can approach the levels needed to challenge legacy gas boilers and CHP systems under the right market conditions.

Under the right market conditions, and through the right commercial partnerships to navigate CapEx and integration hurdles, these technologies can become viable alternatives to fossil-fuelled heat generation. To make higher-temperature electric heat commercially viable by 2030, the sector needs more demonstrators, live labs and corporate-led pilots that prove performance, reduce integration risk and create bankable deployment models.

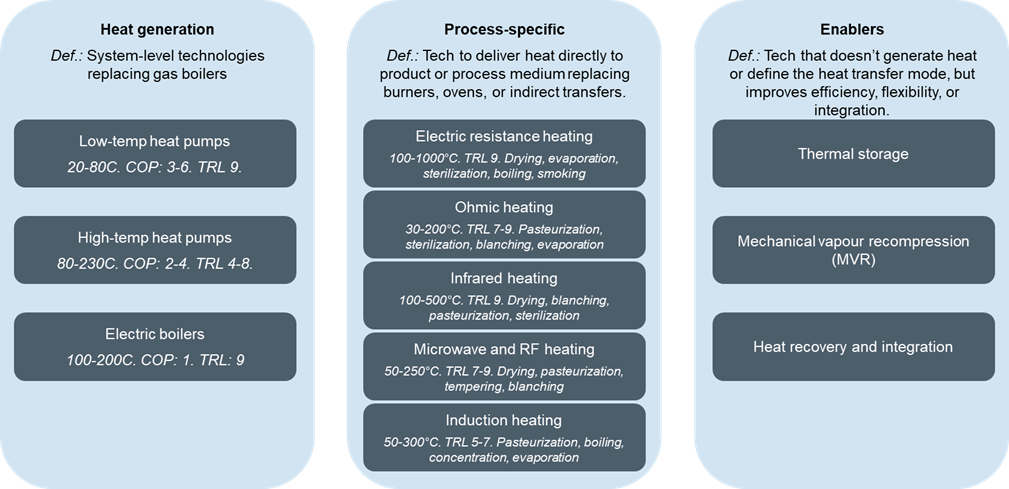

Full-site decarbonisation requires the acceleration of three technology groups

F&B’s lower-temperature heat profile, mostly 150-200°C, makes electrification realistic. But full-site decarbonisation will require a portfolio of technologies, not a single solution.

Many of these methods are achievable, with the right partnerships and commercial models, by 2030, when most corporates have set their Scope 1 decarbonisation targets. The immediate challenge will be enabling the higher-temperature processes and high-temperature heat pumps, with portfolios of heat generation, process-specific, and enabling technologies acting in harmony to deliver zero or low carbon heat.

Beyond 2030, manufacturers will turn to novel R&D pathways to focus on the hardest 10-15% of heat demand, where decarbonisation may be achievable through direct electrification, hydrogen, or zero carbon heat sources. These pathways are outlined by Thiel & Stark (2021).[7] Even today, in some scenarios, low carbon fuels have been made commercial to decarbonise process heating, as evidenced by AstraZeneca’s partnership with biogas innovator Future Biogas to fund their scale-up and secure offtakes.[8]

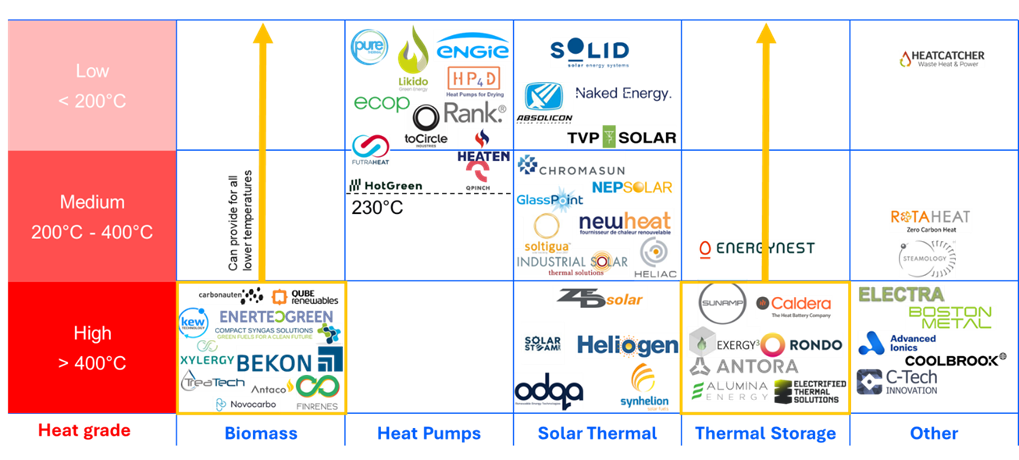

With that in mind, when it comes to innovation, there is no shortage of innovators seeking to commercialise their technologies. In the UK alone, industrial process heat is well represented by the innovation landscape across temperature ranges.

CLT can help Food & Beverage manufacturers convert industrial heat innovation into targeted R&D, partnership and growth opportunities

CLT’s role is to help F&B companies navigate these options and accelerate real-world solutions. We combine technical insight and innovation partnering to bridge the gap between ambitious net-zero heat goals and the practical reality on the factory floor. CLT supports engineering and sustainability teams by:

- Detailing the state of mature vs emerging technologies relevant to their specific process needs.

- Pinpointing “hard heat” challenges (e.g. where COP or integration is problematic) and the R&D partnerships or pilot projects that could unlock solutions.

- Structuring innovation collaborations – from technology scouting and startup partnerships to joint trials, consortia and demonstrators – that enable corporate engineering teams to de-risk and implement novel heat solutions.

By translating heat innovation into credible deployment pathways, CLT helps F&B companies move from insight to action – bridging today’s gaps so that decarbonising process heat becomes an opportunity for improved efficiency, resilience and sustainability, rather than an insurmountable technical problem.

We would welcome the opportunity to discuss how CLT could support your industrial heat and wider cleantech innovation priorities.

Contact

Ben Lynch, Chief Commercial Officer

Ben.lynch@carbonlimitingtechnologies.com

+44 (0) 7980 285393

[1] RTC (2023). Playbook for Decarbonizing Process Heat in the Food & Beverage Sector.

[2] Arthur D. Little (2024). Decarbonizing industrial heat to face climate change

[3] Decarbonising the European Food and Drink Sector: A Net Zero Roadmap

[4] Elwardany et al. (2026). High-temperature heat pumps for industrial decarbonization: Technologies, integration strategies, and future perspectives

[5] Project 68 – Industrial High-Temperature Heat Pumps, Task 1: Technologies, 2025 – HPT – Heat Pumping Technologies

[6] UK Energy Research Centre (2025). Electrifying Industry and Distribution Networks: Considerations for Policymakers

[7] Thiel & Stark (2021). To decarbonize industry, we must decarbonize heat

Written by